The Fed just cut rates again — for the second time this year. And I know what you’re thinking: “Rates are down — is it finally time to buy a house?” But hold up — not so fast. Just because the Fed is cutting rates doesn’t mean it’s time to go all-in on real estate. If you buy the right type of home, great, you’re in a strong position. But if you pick the wrong one, you could end up holding the bag.

So in today’s article, here’s what we’re going to cover: First, what the Fed’s October rate cut really means for your mortgage. Second, the latest data from Seattle’s housing market. Third, what I expect over the next one to two years. And finally, which homes you should avoid right now — and which ones might actually be worth buying. Alright, let’s get into it.

📉Interest Rate and Monthly Payment

On October 29th, the Fed cut rates again — another 25 basis points — bringing the benchmark down to 3.75 to 4 percent.

Most people don’t realize this, but mortgage rates don’t drop overnight when the Fed cuts. It’s more like a slow chain reaction. When the Fed cuts rates, money becomes cheaper, large investors move cash from short-term money markets into long-term bonds like the 10-year Treasury, and that pushes bond yields lower. Mortgage rates usually follow that direction, so yes, the trend is down, but it takes time.

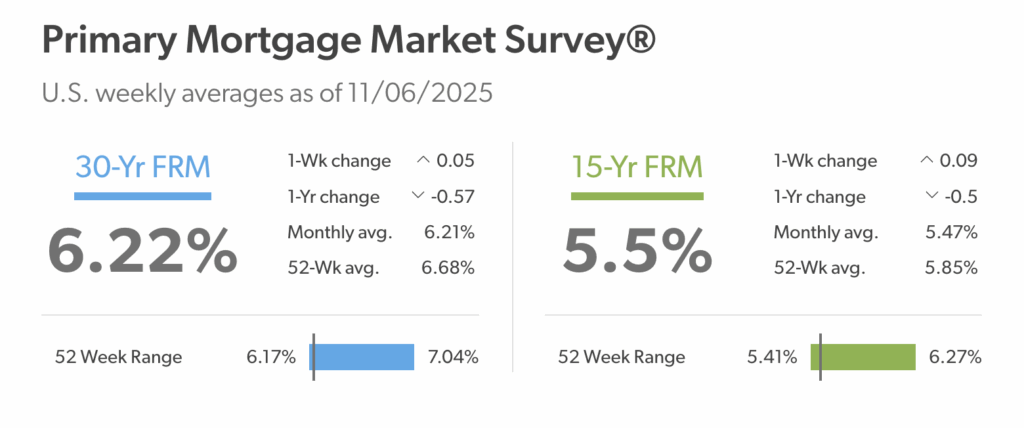

Right now, according to Freddie Mac’s data from November 6th, the 30-year fixed mortgage rate is about 6.22%, down from roughly 7% earlier this year. If you go with a 15-year or ARM, it’s around 5.5%. For a $1.2 million home, 20% downpayment — at 6.5%, your monthly payment is around $6068. Drop that to 5.5%, and you’re paying about $5451. That’s a $617 difference every month, or about $7400 a year — REAL savings.

So yes, it makes sense that buyers are coming back. Real estate is still one of the best long-term hedges against inflation. But — and this is important — don’t go out and buy blindly. Seattle’s market is very uneven right now. Some areas are fairly priced, some are way overvalued, and if you buy the wrong one, you could be stuck for years.

🔥October Data Recap

Now let’s talk about what’s actually happening in Seattle. People keep saying “the market’s heating up again,” so let’s look at the numbers. After the Fed’s cuts and the summer slowdown, October looked better — not a boom, but a clear improvement.

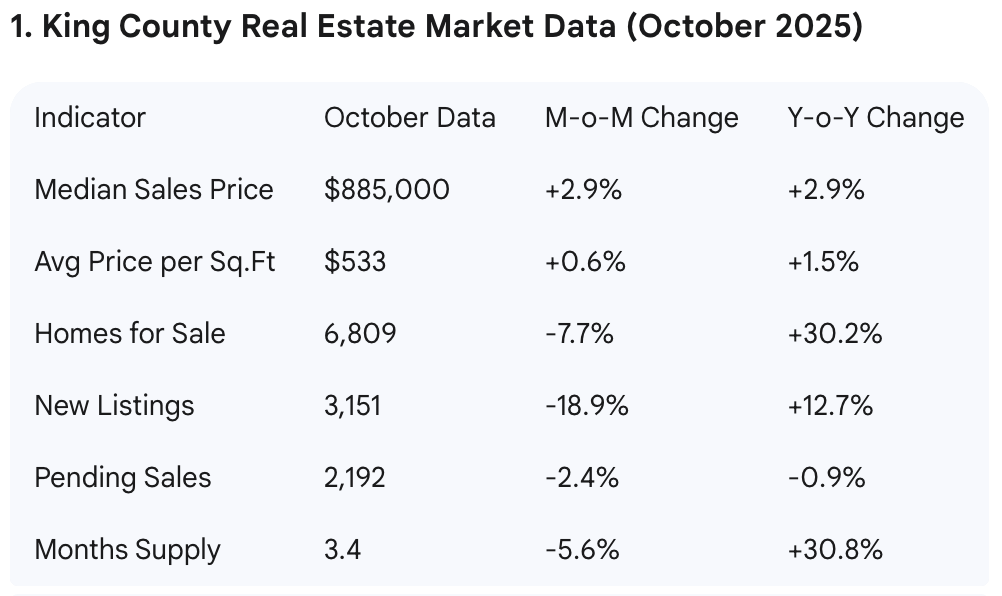

In King County, the median home price hit $885,000, up 2.9% month over month and 2.9% year over year. Price per square foot is $533, up 0.6%. New listings dropped almost 20% to 3,151 homes, pending sales reached 2,192, and active inventory dropped to 6,809 homes — roughly 3.4 months of supply.

So fewer listings, more deals getting done, and a small price rebound — a healthier market than what we saw this summer.

Seattle city’s median price was $900,000, up 5.4% from September and 3.3% year over year. Price per square foot stayed flat, and 826 homes sold — 4% more than last month.

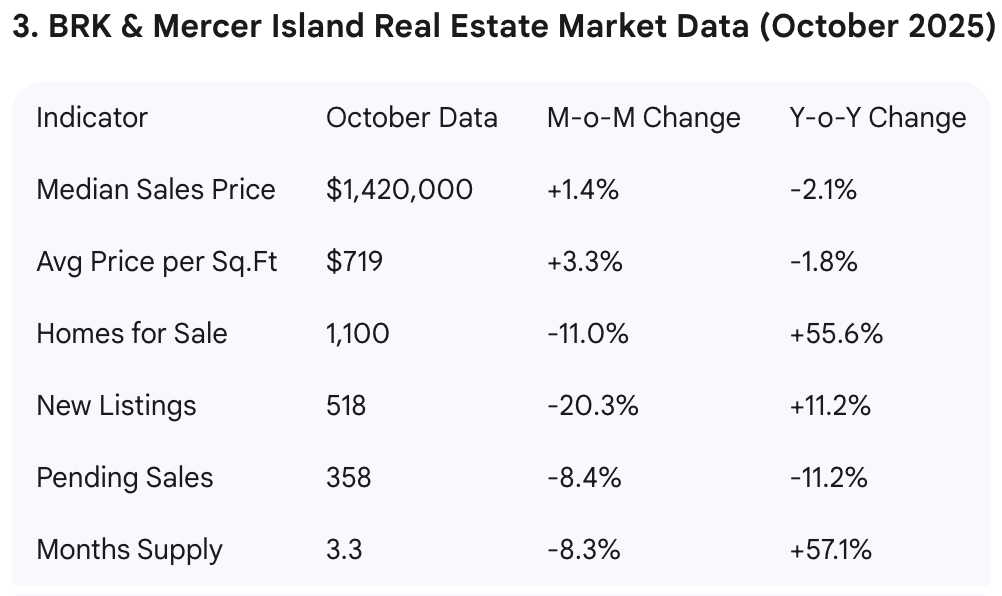

On the Eastside — Bellevue and Mercer Island — the median price hit $1.42 million, up 1.4%, and price per square foot jumped 3.3% to $719. So much for the idea that luxury homes aren’t selling — they are, but sellers are getting realistic.

One of my clients listed their Bellevue home at $1.6 million, then dropped $80,000 and even offered to cover closing costs — not because it couldn’t sell, but because they wanted to close before year-end.

So yes, activity is picking up. Why? Three main reasons. First, rate cuts and the expectation of more cuts gave buyers confidence. Second, fewer new listings — many sellers decided to wait until spring. Third, seasonality — after summer vacations, families want to move before the holidays.

So overall, October’s data shows a market that’s stabilizing, not exploding, but improving.

🔍Future Market Forecast

Now let’s talk about what’s next. Over the next one to two years, Seattle’s housing market will probably stay flat, maybe up a few percent. But long-term, real estate is still one of the strongest assets you can own.

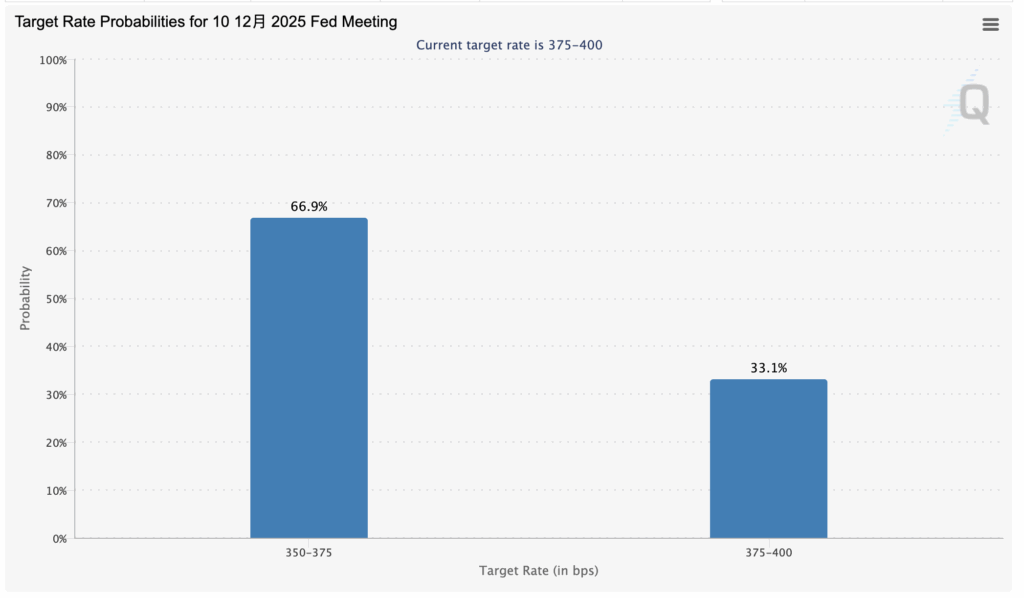

Based on the CME FedWatch Tool, there’s about a 70% chance of another cut in December and another small cut early next year. Fannie Mae expects that by 2026, the 30-year mortgage rate will drop

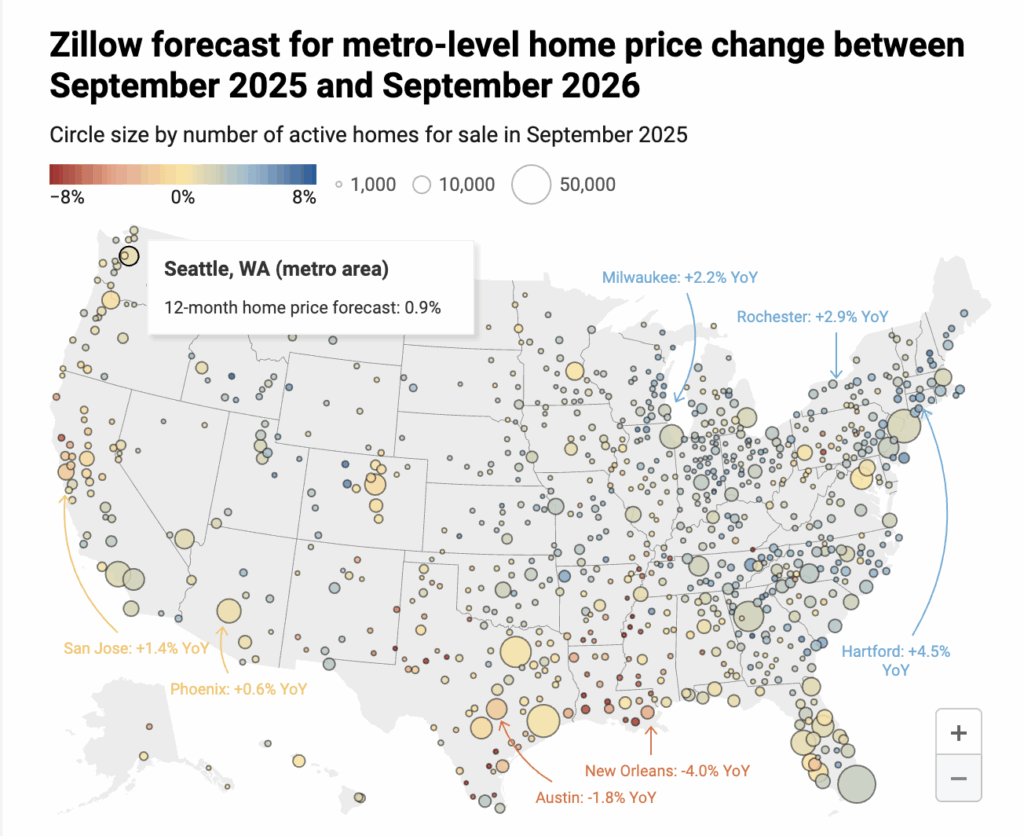

As for prices, Zillow’s outlook has completely flipped this year. At the start of 2025, they were expecting a 1.7% decline. By August, the forecast moved up to +0.4%, then +1.2% in September, and now, in October, it’s +1.9%. There’s only one message here: buyer confidence is coming back.

For Seattle specifically, Zillow expects 0–1% growth next year — and honestly, that’s pretty realistic. We still have a lot of inventory waiting to hit the market, so I’d expect prices to stay mostly flat, maybe 2–3% growth at most.

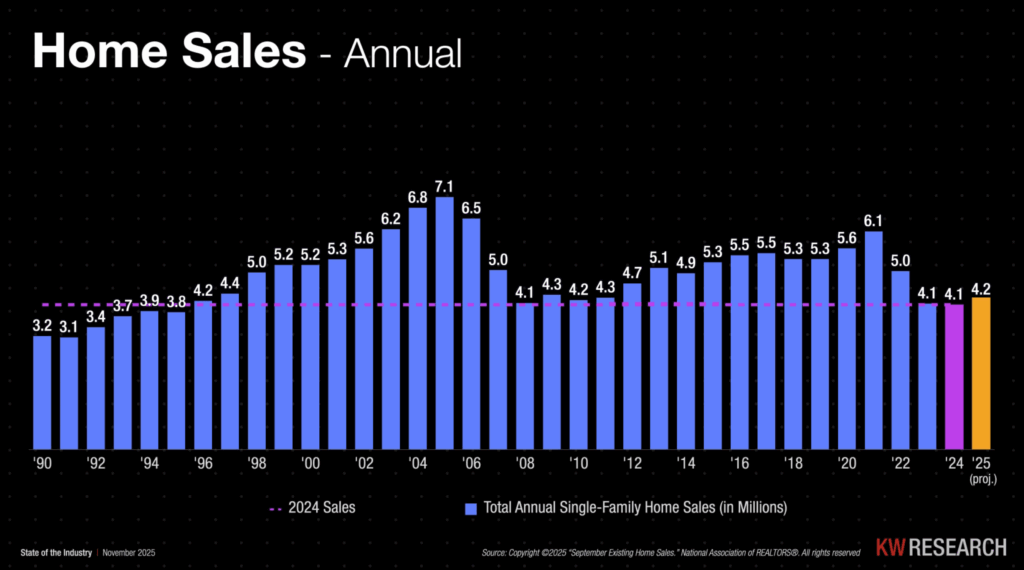

I also attended a housing lecture this week, and the speaker shared an interesting data point: After the 2008 financial crisis, U.S. home sales dropped to the 4.1–4.5 million range for four years — and then the market moved into a new cycle. Today, we are already in the third year of a slowdown, which means the next 1–2 years could very likely mark the beginning of another cycle.

And when you zoom out to the 50-year national home price chart, the trend is very clear. Yes, we had the 2008 crash. Yes, we had the 2022 rate shock. But every correction eventually returned to an upward path. Over the long run, U.S. home prices have grown at a stable 4% per year on average.

⚠️Advices for Buyer and Seller

First, here’s some advice for buyers: in the current market, you should be cautious about avoiding these three types of properties.

First, avoid homes in poor locations. Right now, the market is more divided than ever, and location is the only thing that truly holds value. Avoid homes that are far from major transit, job centers, or daily amenities — if it takes more than 20 minutes to reach key transit hubs, or over an hour to get to Seattle or Bellevue, skip it. Even if the price looks attractive, you’ll struggle to resell later.

Second, avoid properties with high HOA fees. We’re seeing many condos sit on the market simply because the HOA is too high. For example, an $800,000 condo with a $1,000 monthly HOA instantly turns buyers away. When evaluating a condo, look at the HOA-to-value ratio — ideally the HOA should stay under $0.50–$0.80 per square foot. Anything higher makes both ownership and resale more difficult.

Third, avoid listings that are overpriced and unwilling to negotiate. Some sellers are still pricing homes like it’s 2022. These units usually have room for negotiation. But if you try to negotiate and the seller refuses to come down to a reasonable number, just walk away. In today’s market, there will always be well-priced options worth your time.

Now, here are three kinds of homes worth considering.

First, homes that have been on the market more than 30 days — those sellers are motivated. We’ve had clients get great deals after the first price drop. One condo downtown dropped $30,000, and after follow-up, we got another $20,000 off — $50,000 saved.

Second, sweat equity homes — the ones you can improve. One of our team members bought a lake-view home in Renton, renovated it, added an ADU, and boosted the value significantly. That’s how you create appreciation yourself. Third, new construction with builder discounts. Right now, developers are cutting prices to move inventory. A new townhome near me dropped from $1.3 million to $1.1 million, and another community south of Seattle is selling at around $350 per square foot — close to build cost.

Always bring your own buyer agent when visiting new homes; they can negotiate credits or upgrades. One of our clients got $35,000 in credits on top of a discount — that’s effectively $980,000 net on a $1,015,000 home.

🎯Key of Selling a Home: Accurate Pricing

Now for my sellers — Seattle’s market will likely stay flat for a while. If you want to sell fast and get a good price, you have to price it right. Buyers today are data-driven; they know the comps. If you overprice, even by $10,000 or $20,000, your listing could sit for months, and the longer it sits, the lower your final price will be.

So be realistic, price based on today’s market, not 2022’s. If you’re not sure what that number is, reach out. My team can run a pricing analysis, show you the data, and build a marketing plan to help you sell faster.

Because at the end of the day, success in real estate isn’t about timing the market — it’s about understanding it.

So here’s the bottom line: The Fed’s cutting rates, but that doesn’t mean buy everything. Seattle’s market is stabilizing — not booming, not crashing. Over the next year or two, prices will probably stay flat.

If you’re buying, focus on value and long-term potential. If you’re selling, price smart and stay flexible. And if you’d like to see the full October data for Seattle, I’ve put it all together for you. Just click the link below.

I’m Maggie — see you in the next article.

🌟 Connect with Maggie Sun Real Estate 🌟

For the fastest response, visit our website and fill out the contact form:

🌐 https://maggiesunre.com/contact-us/

📱 Call/Text: 425-615-8293

📧 Email: maggie@maggiesunre.com